Finance: How to Build a Strong Money Foundation This Year

Money management isn’t just for investors, business owners or financial experts – it’s for everyone. Whether you’re a student, a working professional, or planning to start a side hustle, understanding the basics of finance can completely change your future.

Today, financial success isn’t about making more money – it’s about managing what you have. In this blog, we will break down the fundamentals of personal finance in a simple, relevant, and actionable way.

Why understanding finances is important today

This year is a rapidly changing world. Inflation, side hustles, AI jobs, online investments – everything moves quickly. If you don’t manage your money consciously, you’ll always feel like you’re “earning but not saving.”

Learning Finance helps you:

- Control your spending

- Save more without sacrificing comfort

- Invest early and build wealth

- Be prepared for emergencies

- Create a stress-free financial life

1. Start with the 50-30-20 money rule

Start by checking your pay statement. Deduct only the taxes that have been withheld from your total earnings. Don’t eliminate other automatic deductions, such as health insurance or retirement contributions, as these should be included in your budgeting process.

This is one of the simplest budget systems:

- 50% Necessities: Rent, Groceries, Bills

- 30% Necessities: Eating out, Shopping, Subscriptions

- 20% Savings/Investments: FD, SIP, Mutual Fund, Emergency Fund

You can use apps like Walnut, ET Money, GoodBudget, or even Google Sheets to track your daily expenses.

2. Create an emergency fund

An emergency fund is a collection of money set aside to cover unexpected expenses such as medical expenses, home repairs, or sudden loss of income. These funds should be kept separate from your regular spending money to ensure they are available when you really need them.

Life is unpredictable – job loss, medical bills, business losses, or sudden expenses can come at any time.

Save at least 3-6 months of your monthly expenses.

Keep it in:

- Savings account

- Liquid fund

- Short-term FD

It gives you peace of mind and financial stability.

3. Start investing early (even small amounts are important)

You don’t need ₹1,00,000 to start investing. Even ₹500-1000 per month in a SIP (Systematic Investment Plan) is enough. This only emphasises that time is more valuable than any other treasure, because once time is gone, no wealth can bring it back.

Beginner-friendly investments:

- Index Funds (Nifty 50) – Safest for Beginners

- Mutual Funds (SIP)

- PPF

- Government Bonds

- Recurring Deposit (RD)

The goal is consistency, not a large amount of money.

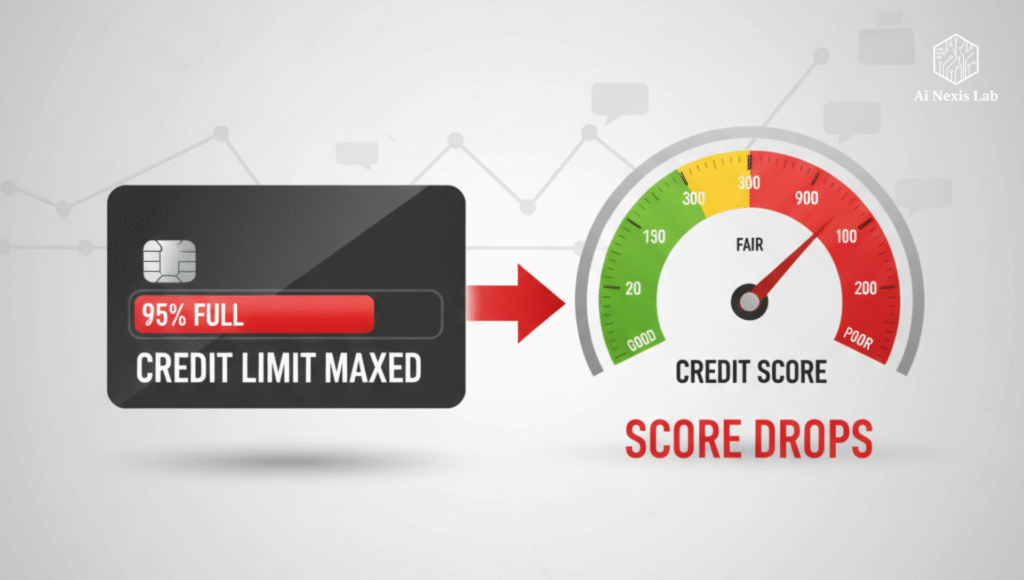

4. Use credit cards wisely (not emotionally)

Using credit cards wisely means treating them as financial tools – not as emotional comforts. It’s easy to swipe a card when you’re stressed, excited, or tempted by a sale, but emotional spending often leads to high balances and unnecessary debt. Instead, use your credit card purposefully. Plan your purchases, track your expenses, and only charge what you can afford each month. Create healthy habits like avoiding impulse purchases, reviewing statements regularly, and keeping your usage low. When used responsibly, credit cards can help you build credit, earn rewards, and support your financial goals without creating additional stress.

Credit cards are powerful tools if used correctly.

Good practices:

- Pay in full on time

- Don’t buy things you can’t afford

- Use cards for cashback and offers

- Keep usage under 30%

Avoid:

- Minimum Payment

- Multiple EMIs

- High Interest Purchases

A good credit score helps you get loans easily in the future.

5. Track Your Net Worth Every Month

Tracking your net worth each month helps you understand your true financial progress. It shows the difference between what you own and what you owe, giving you a clear picture of your overall stability. By updating it regularly, you can spot trends, celebrate growth, and adjust your habits if needed. Monthly tracking also keeps you motivated, helping you stay consistent with saving, investing, and paying down debt. It’s a simple practice that brings long-term clarity and confidence to your financial journey.

Your Net Worth = Assets – Liabilities

(Assets = Savings, Investments; Liabilities = Loans, EMIs)

When you track it on a monthly basis, you automatically become more disciplined with money.

6. Learn One New Finance Skill Every Week

Learning a new financial skill every week is a powerful way to strengthen your mindset towards money and build long-term confidence. Whether it’s understanding interest rates, budgeting better, improving your credit score, or exploring basic investing, small weekly lessons quickly add up. This habit keeps you curious, informed, and better prepared to make smart financial decisions. Over time, you will develop a strong foundation that will help you manage money wisely, reduce mistakes, and move closer to your financial goals with steady growth.

Here are easy topics to learn:

- What is compound interest?

- How do mutual funds work?

- What is an index fund?

- What is inflation?

- How does credit score affect loans?

The more you learn, the smarter your decisions become.

Frequently Asked Questions (FAQ)

Q1: Why is it important to have a financial foundation?

A strong financial foundation helps you stay in control of your money, avoid debt stress, and be prepared for emergencies, big goals, or retirement. It gives you flexibility and peace of mind when unexpected expenses or life changes occur.

Q2: How should I start – should I budget or save first?

Start with a simple budget. Keep track of your income and expenses to know where your money goes. Once you have clarity, you can start saving – even small amounts are important. Over time, you can steadily increase your savings.

Q3: How much should I save each month / How big should my emergency fund be?

A good rule of thumb is to gradually build an emergency fund that can cover 3-6 months of your essential expenses. But don’t wait too long – even small, regular savings are better than waiting for the “perfect” time.

Q4: Should I focus on paying off debt or saving first?

Ideally, do both – but prioritize high-interest debts first (like credit-card debt), as interest adds up quickly and can eat into your savings capacity. Once high-interest debt is under control, put more money towards savings and investments.

Q5: Is it important to invest or should I just save money in a bank account?

Savings are important for short-term goals and emergencies because they are safe and liquid. But investing becomes useful for long-term goals – helping to grow your money, outpace inflation, and build wealth. Once you have a stable financial base (budget, emergency fund, manageable debt), you can start investing.

Summary

Finance is not complicated – it just requires continuous education and a little discipline. Start small, understand your habits, and slowly build your financial future. Remember: wealth grows over time, not through shortcuts.